The 2026 Federal Budget and Australian Property: What's Really Changed

Share this post

When the Treasurer rose at 7:30pm on 12 May 2026, most Australians watching at home didn't realise they were witnessing one of the largest structural shifts to residential property investment in a generation.The headline measures, quarantining negative gearing on established homes, full exemptions for new house and land packages, and grandfathering of existing arrangements … sounds technical however, consequences are not.

For investors, this Budget has redrawn the map. Not just the rules, but the entire risk-and-return calculus of where capital should flow. This article goes deeper than the headlines and we unpack what has changed, why theGovernment made the choices it did, what the market is already telling us, and how the maths now genuinely favours new builds over established stock in a way that wasn't true even six months ago.

What Actually Changed: The Legislation in Plain English

The 2026 Federal Budget introduces three core changes that take effect from 1 July 2027. Negative gearing on established residential properties will be quarantined. This is the headline change and it deserves precise language. Under the existing system, if your investment property runs at a loss say, your rental income is $31,000 but your interest, depreciation, and holding costs total $55,000 that $24,000 loss can be deducted against your other taxable income, including your wage or salary. For a high-income earner on the 47% marginal rate, that produces a tax refund of more than $11,000 in the year the loss is incurred.

From 1 July 2027, that loss is no longer off setable against unrelated income. Instead, it's quarantined: carried forward indefinitely and only applied either against future profits from the same property (or other investment properties), or at the point of sale to reduce capital gains tax.The deduction isn't gone, it's deferred.But for most investors, the cashflow impact is immediate and substantial.

Grandfathering for existing arrangement

New house and land packages are fully exempt. Any new build defined as a property that has not previously been occupied retains the full existing treatment. Full negative gearing against PAYG income, full depreciation schedules on building and fixtures, and the ability to access immediate tax refunds on holding costs. The Government has effectively created a two-speed property market by policy design.

Any contract signed before 7:30pm on 12 May 2026, the moment the Treasurer began the Budget speech is grandfathered under the current rules.Properties owned under existing contracts retain full negative gearing rights indefinitely, including through future refinancing.

Why The Government Made These Choices

This isn't an accident of policy. The Treasury position, articulated in the Budget papers, is that Australia faces a housing supply crisis and that the existing negative gearing settings encourage capital to flow into bidding up the price of existing stock rather than financing new construction. By preserving the tax advantages exclusively for new builds, the policy directs investor capital toward developers and builders the actors who can actually increase the supply of housing. It's a structural lever pulled in service of a structural problem.

You can debate the policy on its merits. What you cannot debate is its existence. And what investors need to understand is that this isn't a temporary intervention. It's a permanent reshaping of where the returns sit.

The Market Is Already Moving

The market has not waited for 1 July 2027. It has begun pricing the changes immediately.CBA's forecasting team has published modelling suggesting house prices in segments with high investor participation will land approximately 3% lower than they otherwise would have, driven by reduced investor demand for established stock. The 3% headline number understates the segmentation: in suburbs where investors represent more than 40% of buyers, the impact is meaningfully larger.

Cotality's data shows Sydney and Melbourne entering early decline phases even before the changes take effect, with affordability pressure and the prevailing rate environment compounding the impact of the Budget signal. Brisbane, Perth and Adelaide remain comparatively resilient but are not immune. What this means practically: the established stock investors are most familiar with inner and middle-ring metropolitan houses and units is the segment most exposed. The properties offering the best long-term capital growth historically are also the ones most affected by the policy shift.

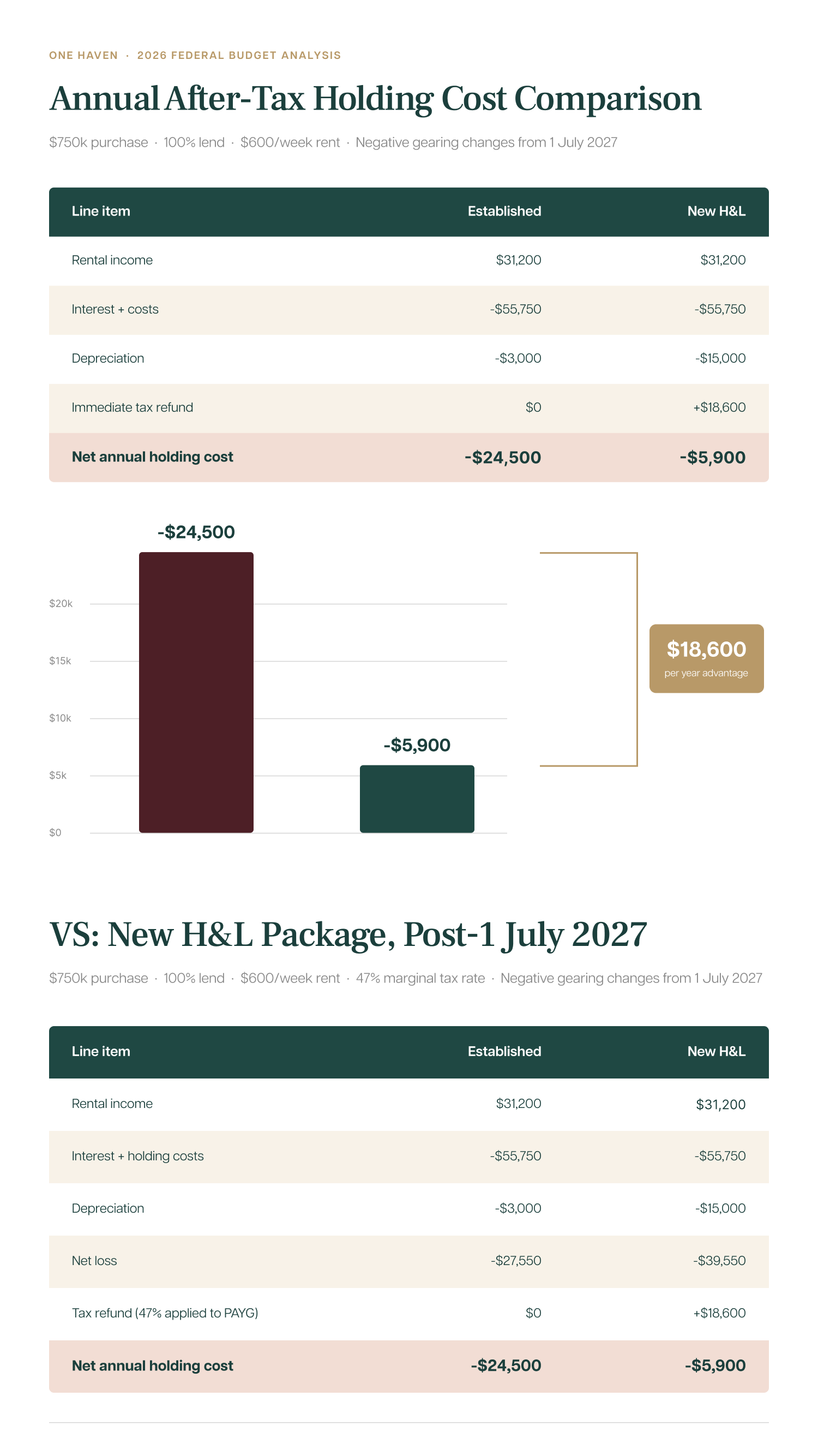

The Numbers: An Extended Worked Example

The hypothetical example in our earlier briefing showed the after-tax cashflow gap between an established property and a new H&L package. Here we extend that analysis for the first year after establishing the investment property:

Lets assume the same setup: a $750,000 purchase price, 100% lend,$600/week rent ($31,200 annual gross income), and an investor on the 47%marginal tax bracket (income above $250,000 including Medicare levy).

Why The Gap Compounds Over Time

The single-year analysis understates the long-run impact for two reasons. First, depreciation schedules on new builds are front-loaded. The first five years of depreciation deductions on a new H&L package are materially higher than years six through ten, which means the early cashflow advantage is even larger than the steady-state figure suggests. For an investor still in the wealth-accumulation phase, those early years of retained cashflow are the most useful. they're the years that fund the next purchase.

Second, the established-property investor's quarantined losses do eventually become useable, but only on disposal or against future property profits. For a long-hold investor and most residential investors hold for at least 10 years that's a deferred benefit that fails to compound. Cash today funds tomorrow's deposit. Cash deferred to a future sale doesn't. The result is that the gap between the two investment strategies doesn't stay constant. It widens.

The New Build Premium: Why It Still Stacks Up

The most common pushback we hear from sophisticated investors is straightforward: new builds carry a premium. You're paying more per square metre, often in less-established locations, and the capital growth profile is historically slower than well-located established stock.

The premium for a new H&L package, typically 8% to 15%above comparable established stock, has to be evaluated against the structural cashflow advantage and the depreciation benefit, not just against capital growth in isolation. A property that costs 10% more but delivers $18,600 in additional annual cashflow is, on a total-return basis, a different asset class. You're not paying more for the same outcome. You're paying more for a measurably different financial profile.

The other piece sophisticated investors often miss: the established-property capital growth premium that historically justified the higher cost was substantially driven by investor demand. When investor demand exits a segment, as it is now doing, the historical capital growth premium begins to compress. You may be paying for a growth profile that the policy change itself is now eroding.

What This Means For Other Asset Classes

This is where the conversation goes beyond residential property. Investment capital is fungible. If the after-tax return one stablished residential is structurally lower, capital flows elsewhere, to equities, to commercial property, to overseas allocations, to new build residential.

The tax-adjusted return on a new H&L package, for a high-income investor, now meaningfully exceeds the tax-adjusted return on a comparable established property and, in many cases, exceeds the after-tax return on a diversified equity portfolio when the leverage advantage is factored in. That's a strong statement. It's also the position the post-Budget arithmetic supports. New build residential property is, for the next decade at least, structurally advantaged as an investment vehicle in a way it has never been before.

What The Sophisticated Investor Does Now

Three observations for investors weighing their next move. First, the window to take advantage of grandfathered arrangements has closed. If you didn't have a contract signed before 7:30pm on 12 May 2026, that ship has sailed. Don't anchor decisions to a regime you can no longer access.

Second, established stock should be evaluated under the new tax rules, not the old ones. Spreadsheets and models built on pre-Budget assumptions overstate the after-tax return on established residential. Update them!

Third, quality matters more, not less. The new build segment is going to attract a wave of capital, and not all stock is equal. Volume builders in poor locations will not deliver the returns the policy framework theoretically enables. The investor who selects well-located, well-built new stock, typically off-market or limited-release, captures the policy advantage. The investor who buys whatever's available in a release park does not. This is where the conversation moves from policy analysis to execution. The Budget has changed the rules. What you do next determines whether you benefit from the changes or watch others benefit while you wait.

Closing Thought

Budgets are usually narrative events. They produce headlines, they produce some short-term political theatre, and then the market absorbs them. The 2026 Federal Budget is different. It has reset the underlying maths of residential property investment in Australia, and the reset is permanent.

The investors who recognise the shift and act on it will look back in a decade and describe this period as obvious in hindsight. The investors who treat it as another piece of policy noise will look back and wonder how the gap got so wide. The maths is not ambiguous. The direction is not ambiguous. The only question is whether you act on what the numbers are telling you.

View more from the Haven Hub

Real stories from the people we’ve helped, sharing their experiences, outcomes, and the impact we’ve made along the way. These insights reflect our commitment to delivering results that genuinely matter to our clients.

Why you should invest in property

Apart from purchasing a property and seeing the uptick in value over time, there are additional financial incentives and benefits that – if you buy well – arise as part of the process of investing in property.

The value of patience in property investment

Like most successful investment strategies, time and patience are two key factors when it comes to achieving solid returns on the property market.

Key terms to understand before you start investing in property

When you first start thinking about investing in property, it can seem a bit daunting…but you shouldn’t let that get between you and your first investment!

Property investment 101: Your go to guide before getting started

Property investment 101 will demystify property investment for you! So before you get started buying, make sure you take a few minutes to finish reading!

.webp)

Strong Finish to 2025 Sets the Stage for the Year Ahead

The Australian housing market wrapped up 2025 on a remarkably strong note, a trend that provides invaluable insight as you consider your investment moves for 2026.

Considerations of property investment within a SMSF

Relying on your super alone for a comfortable retirement might not be enough, especially if you’re planning on retiring early or still supporting a family. That’s why making investment decisions sooner rather than later in life can make a massive difference to your overall circumstances in retirement! And using a Self-Managed Superannuation Fund (SMSF) to build wealth effectively is something that many Australians are yet to fully leverage.

No pressure

No jargon

Just clear advice and ongoing support from people who genuinely care.